Where Did My Rent Actually Go This Month?

Your PM collected $1,600.

Your bank account got $1,120.

Nobody stole $480. Probably.

That is the annoying part. The money usually did not vanish. It got renamed. Management fee. Repair. Reserve top up. Leasing charge. Owner contribution. Timing item. A line on the statement with a name so boring your brain skips it.

That skipped line is where owner cash goes to hide.

If you use a property manager, the question is not “how much rent did the tenant pay?” The question is where the rent went after your PM collected it.

The rent did not vanish. It got renamed.

Rent collected is the top of the month.

Owner payout is the bottom.

Everything between those two numbers is the actual story.

Here is the tiny version:

- Rent collected: $1,600

- Management fee: $160

- Repair: $220

- Reserve top up: $100

- Net payout: $1,120

That $480 is not a mystery. It is the middle of the statement.

The problem is that most owners glance at the net payout, compare it to the mortgage, sigh, and file the PDF. “Looks lower than usual” becomes the entire audit.

Great. A forensic method invented by vibes.

The owner statement should tell you exactly how the month moved from collected rent to usable cash. If it does not, you do not have a cash flow number. You have a PDF with confidence.

Your owner statement should answer 3 numbers

Every PM statement has one job for the owner.

It should connect 3 numbers.

First, what was collected.

Second, what was deducted or held.

Third, what reached your bank.

That is the owner side money map. Collected. Spent or held. Delivered.

The statement is useful only if the middle is readable. A management fee should match the agreement. Maintenance should tie to an invoice. A reserve top up should show the new reserve balance. A leasing or renewal charge should match the contract.

The Oregon property management trust account rule is written for PMs, not owners, but the principle is useful: bank records, receipts and disbursements, and owner ledgers have to reconcile with each other. One record is not enough.

That is the owner version too.

The PM statement is one record. The bank deposit is another. The agreement and invoices explain the middle.

The bank deposit is proof, not the whole month

The bank deposit proves cash landed.

It does not prove the month was clean.

If the statement says your owner payout is $1,120 and the bank shows $1,120, good. Now look up.

Was the fee calculated on collected rent or scheduled rent? Did a renewal fee get billed like a new lease placement? Did the repair include a vendor markup? Did a late fee appear on the statement but never reach your books? Did the PM hold back a reserve because the agreement allows it, or because someone needed the account to balance?

Matching the deposit is pass one.

Reading the line items is pass two.

Most owners stop after pass one because pass two is boring. That is why it works. Boring money leaks have excellent survival rates.

For a full monthly checklist, use the property manager statement reconciliation guide. For a faster smoke test, run the free PM statement audit.

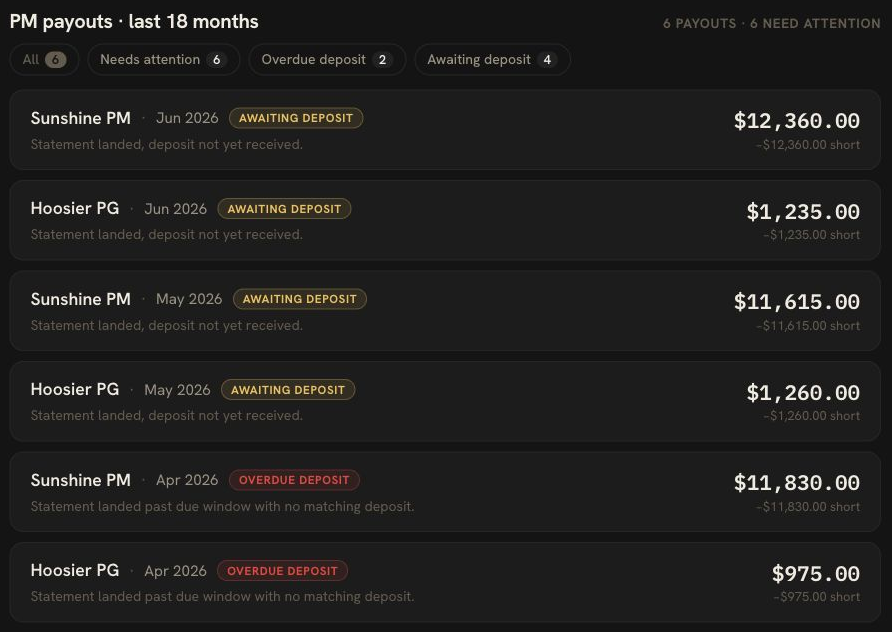

Held money is where owners stop paying attention

The most misunderstood line on a PM statement is not the fee.

It is money held back.

Reserves are normal. Many PM agreements require the owner to keep $300, $500, or one month of expected expenses available for repairs and vacancy. Fine.

The problem is when reserves move quietly.

One month the statement shows a $100 reserve top up. Next month another $100. Then a repair gets paid from the reserve. Then the payout looks thin, but nobody can tell whether cash was spent, held, or already reimbursed.

This is how a property with decent rent starts feeling broken.

Not because the asset failed.

Because the month has 6 places for money to sit and the owner only checks one of them.

DoorVault treats held money as part of the month, not a footnote. PM versus bank reconciliation shows the expected payout, the bank match, and any variance. PM statement processing reads the lines above the payout. Action Center carries weird gaps into a task while the month is still fresh.

Yeah. It is statement math.

That is the point.

DoorVault turns the month into evidence

DoorVault is built for investors who use property managers but still need to run the asset.

Forward any property related email to Knox. PM statements, invoices, insurance renewals, tax bills, mortgage statements, lease packets, inspection reports, anything tied to the property. Knox reads the attachments, files the documents to the right property, and proposes the bookkeeping for review.

For this specific money flow, DoorVault does the boring catch:

- Reads the PM statement line by line

- Pulls rent, fees, repairs, reserves, and net payout

- Matches the expected owner payout to the bank deposit

- Flags missing deposits, short payouts, duplicate charges, and weird reserve movement

- Keeps the statement and supporting documents attached to the property

Manual PM statement review can take 30 to 60 minutes per statement. DoorVault turns that into about 2 minutes of review because the owner is checking exceptions instead of rebuilding the month.

The same clean data feeds the rest of the owner record: per property P&L, Schedule E export, loan and equity context, PM performance, entity reporting, and portfolio decisions.

Not a pile of tabs.

One owner record.

The monthly rent map

Here is the test to run every month.

- What rent was collected?

- What did the PM deduct?

- What did the PM hold?

- What actually hit the bank?

- What document proves each line?

If you can answer those 5 questions, the month is readable.

If you cannot, do not call it cash flow yet.

Call it what it is.

A statement you have not reconciled.

DoorVault is for the owner who wants the PM to run the property, but does not want a PDF to run the asset.

Start free. 2 properties. No credit card. https://doorvault.app

FAQs

Why does my bank deposit not match rent collected?

Your bank deposit is usually net cash after management fees, repairs, reserves, leasing charges, owner contributions, timing items, and other statement activity. Reconcile rent collected to the PM statement, then match the expected payout to the actual bank deposit.

What should I check on a property manager statement?

Check rent collected, PM fee math, maintenance lines, reserve movement, leasing and renewal charges, owner contributions, net payout, and the matching bank deposit. The statement should explain how rent became cash.

How does DoorVault reconcile PM statements to bank deposits?

DoorVault reads the PM statement, extracts the line items, files the PDF to the right property, and matches the expected owner payout to the bank deposit. Knox flags gaps so you review the exception instead of rebuilding the month manually.