Property Manager Bank Account Access Is Where Investors Get Burned

Your property manager asked for bank account access.

Not to view it.

To spend from it.

Most investors answer this one of two ways.

Either they say yes because they want speed.

Or they say no because they have a bad feeling, but they do not have a better system.

This post is the better system.

It is not legal advice. Rules vary by state. Talk to your attorney if you need formal answers.

It is an owner side controls checklist so you can keep speed and keep control.

If your PM needs your bank login, the system is already broken

Investors hire property managers for the same reason they use direct deposit.

They do not want to touch paperwork.

But the moment your PM needs full access to an owner operating account, you are back in paperwork land.

Because you now have to ask one question forever.

Did they spend money the way we agreed.

The scary part is normal work with zero guardrails.

One vendor bill gets paid twice.

One reserve top up happens three months in a row.

One fee changes from 10 percent to 11 percent and nobody emails you.

That is a 1 percent rent haircut. Every month. Forever.

Most investors do not catch it because they are not running a monthly close.

They are reading a PDF once a month and hoping the bank deposit feels right.

You do not need to become your PM accountant.

You need a few controls and a month end loop.

Three types of access that get lumped together

When a PM says “bank access,” ask which one they mean.

These are not the same thing.

1) View only access

They can see deposits and balances. They cannot move money.

2) Deposit only access

They can deposit rents and owner distributions. They cannot pull money back out.

3) Spend access

Debit card. ACH. Checks. Bill pay. Signatory access. Anything where they can move money out.

Only the third one changes your risk profile in a meaningful way.

The goal is not to slow the PM down.

The goal is to define what “normal” looks like before the first weird charge hits.

Here is the operating question to anchor everything.

If the PM can spend from the account, what stops a $200 repair from becoming a $2,000 story.

Your answer cannot be “trust.”

Your answer has to be thresholds, receipts, and a monthly close.

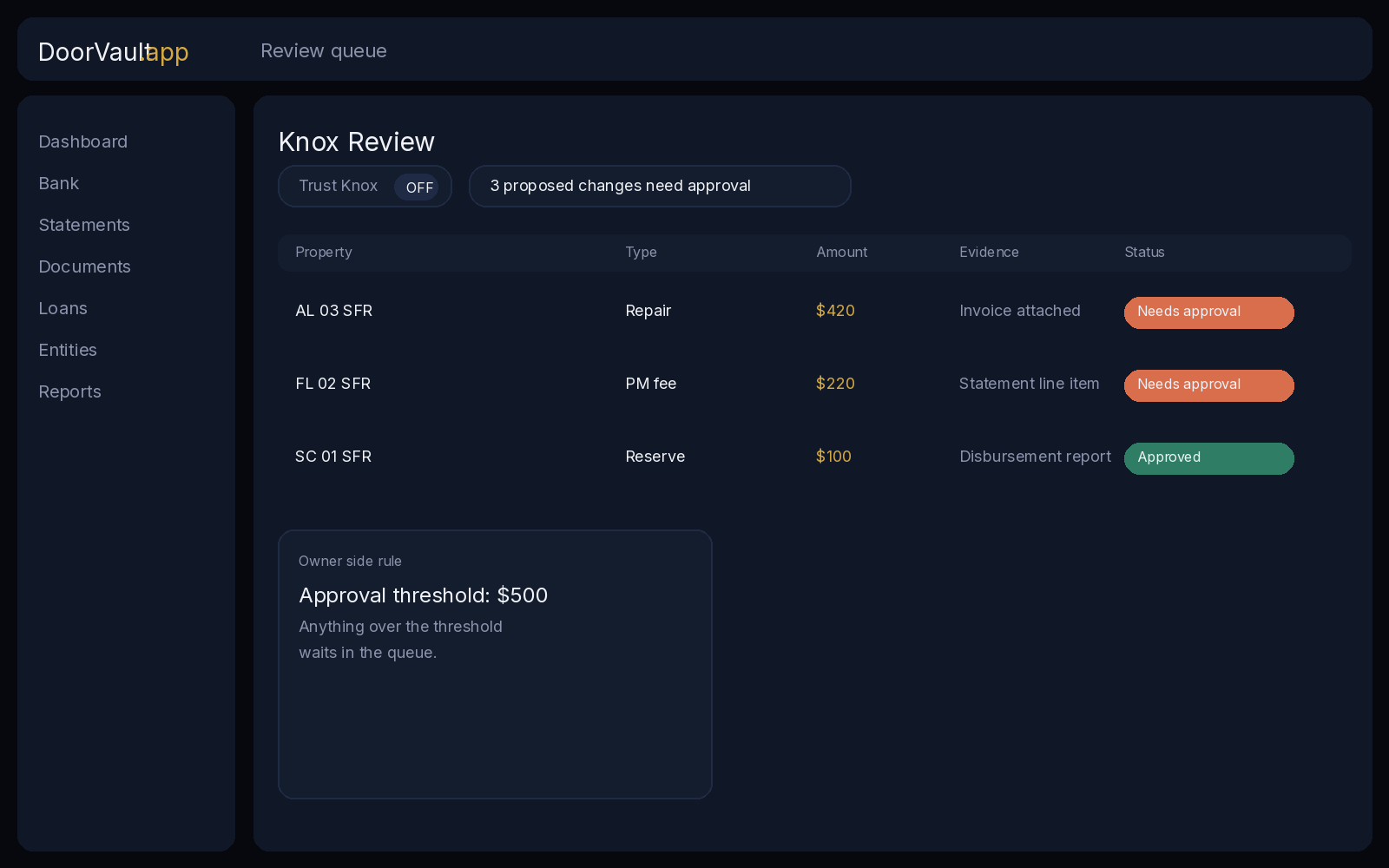

The owner side control checklist (speed without surrendering control)

This is the checklist we recommend for PM managed rentals.

It is boring on purpose.

Boring is where money stays inside the portfolio.

Control 1: A written approval threshold

Pick a number.

$250.

$500.

$1,000.

Whatever fits your asset class.

Then write the rule in one sentence.

Anything over that number needs written approval.

No verbal approvals. No “we talked about it last month.” No “it was an emergency” for a toilet flapper.

If your portfolio has 10 doors, a $500 threshold prevents a lot of surprise $1,800 invoices.

Control 2: Receipt required, tied to the property

Every spend needs a document.

Invoice.

Work order.

Photo.

Something.

If the only proof is a line item on an owner statement, you do not have proof.

You have a rumor with a dollar sign.

This matters because the month end close is not math.

It is evidence.

Control 3: A reserve policy you can explain in 30 seconds

Most “mystery deductions” are not theft.

They are reserve movements.

Define the reserve number per property and the rule for changes.

Example:

Keep $1,500 per property.

If the reserve is used, it gets topped up next month, once, with a note.

That is it.

If the reserve target drifts every month, you have a control problem.

Control 4: A monthly close date

Pick one day.

The 15th.

The last day of the month.

Whatever lines up with your PM.

Put it on the calendar.

Statement.

Bank deposit.

Reserve balance.

If those three do not match, you do not need to panic.

You need an explanation, and you need it in writing.

The month end close loop (statement, deposits, reserves, invoices)

This is the loop most investors never build.

It takes 15 minutes per property, per month, when you do it consistently.

If you do it once a year, it takes a weekend and ruins your mood.

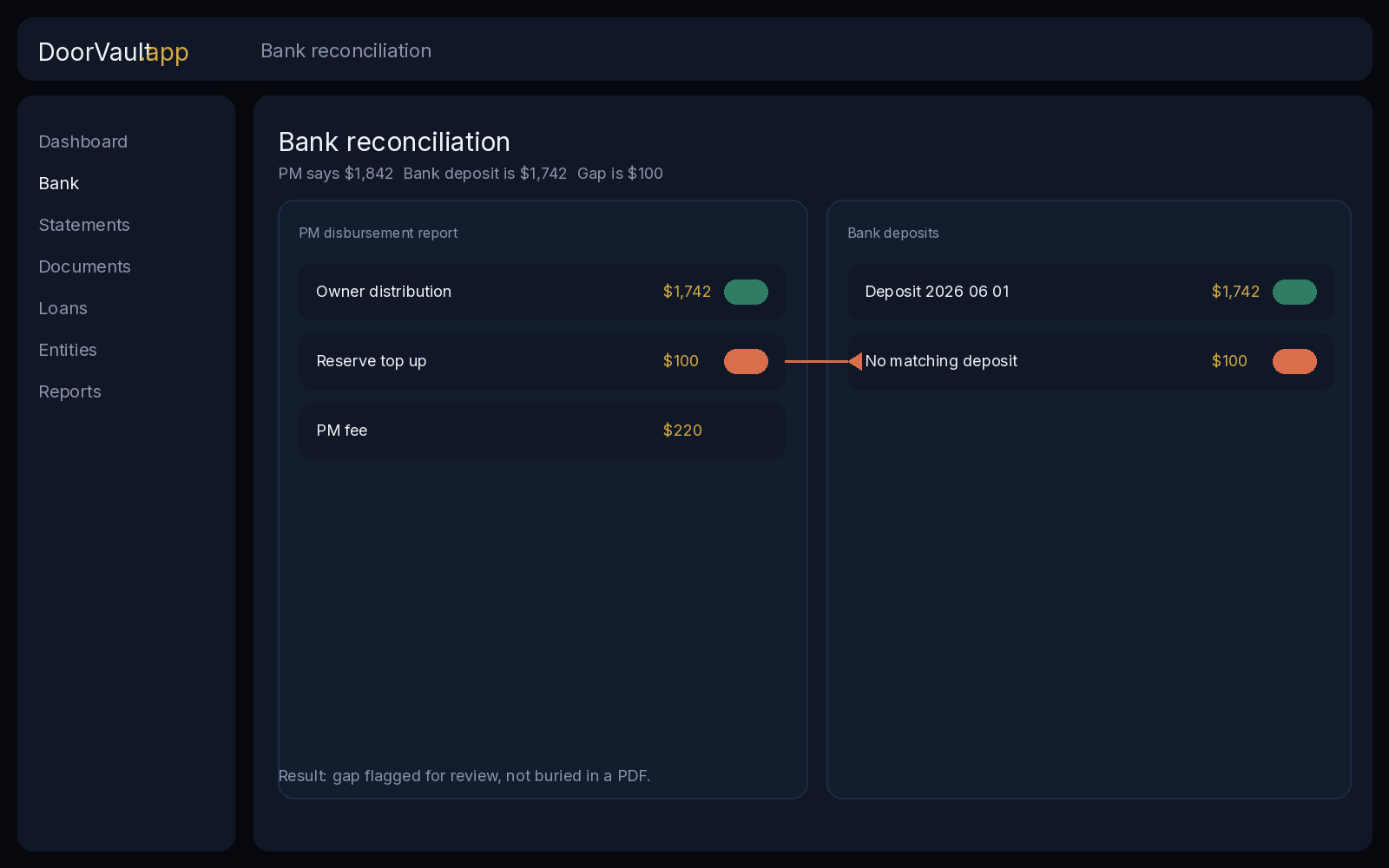

Step 1: Tie owner distribution to the bank deposit

If the statement says $1,842 and the deposit is $1,742, the difference has to be one of these:

- a reserve movement

- a bill paid from collected rent

- a fee

- a timing issue

If you cannot explain the gap in 60 seconds, log it as unresolved.

Step 2: Confirm every repair line has a matching invoice

If the invoice is not attached, ask for it.

Do not accept “vendor name only” as a substitute.

If the PM is paying from your account, you are entitled to the paper trail.

Step 3: Check fee math against the agreement

Fees drift because nobody checks.

The easiest win is to run one percent math:

If rent collected is $2,000, then 10 percent is $200.

If your statement shows $220, that is 11 percent.

Step 4: Track reserves as a separate line item

Reserves are not expenses.

They are cash allocation.

Treat them that way.

Write down reserve start, reserve used, reserve end.

If the reserve end is never stable, your “cash flow” number is fake.

Step 5: Save the evidence where you can find it

Every month end close creates a proof packet:

- owner statement PDF

- invoices and photos

- insurance or compliance docs if they showed up

- your notes on what was approved and why

This is what your CPA asks for.

This is what a lender asks for.

This is what you need when you fire a PM.

Where DoorVault fits (one inbox, one vault, one audit trail, one dashboard)

Most investors end up giving too much bank access for one reason.

They do not have an owner side system of record.

They have a PM portal, an email inbox, and a bank login.

So they hand over control in exchange for speed.

DoorVault is the opposite trade.

Knox Intelligence is AI that proposes, learns, and never touches your data without permission.

You can move faster, but you still stay in control.

Here is what that looks like in practice.

Forward the owner statement, invoice, or insurance renewal to your Knox inbox.

Knox reads it, proposes the bookkeeping, and files the document to the right property.

Trust Knox off means you review before anything changes.

Trust Knox on means the routine stuff applies instantly.

Bank reconciliation ties the statement to the real deposit.

The Activity Log is the audit trail.

The dashboard turns into something you can use.

None of this removes your property manager.

It removes you as the integration layer between portals, PDFs, and bank statements.

FAQ: trust accounts, reserves, and who should hold what

Does a property manager need a trust account

In many states, PMs who collect rent and deposits hold client funds in a separate trust or escrow account and reconcile it. Requirements vary. Read your state rules and your management agreement.

Is it normal for a PM to have spend access to an owner account

It can be normal in some setups. The real question is whether you have written thresholds, receipts, and a monthly close. If the answer is no, spend access becomes expensive fast.

Should I keep a minimum balance for the PM

If your agreement requires it, define the amount per property and the rule for topping it up. A floating reserve target is how “cash flow” disappears.

Who should hold security deposits

State rules vary. Some structures keep deposits in the PM trust account. Some transfer to the owner. Do not guess. Follow your agreement and your state requirements.

The one sentence verdict

If your portfolio needs your PM to have your bank login, you do not have passive income.

You have outsourced the work and kept the risk.

If you want the owner side system that keeps speed and keeps control, start here:

https://doorvault.app