Escrow Shortage on a Rental Property: Why Your Mortgage Payment Jumped (And How to Stop Getting Surprised)

You bought rentals to collect cash flow, not to wake up to a letter that says your mortgage payment just went up by $150 a month.

An escrow shortage is the most common way that happens. Not because you missed a payment. Because your taxes and insurance moved, your servicer ran the annual escrow math, and the update hit your cash flow all at once.

This guide is written for rental owners, especially owners who use property managers. Homeowner advice is fine for one house. It breaks the moment you have multiple properties, multiple loans, and a document trail that gets buried in PM emails.

Why escrow shortages hit rental owners harder than homeowners

If you own one primary residence, an escrow shortage is annoying. If you own 5 rentals across different servicers and counties, it is operational risk.

Here is why:

- Your “payment” is not one number. It is principal and interest plus tax escrow plus insurance escrow. When escrow moves, your cash flow moves.

- The documents do not land in one place. Insurance renewals might go to your agent, tax bills might go to the PM, and escrow analysis statements might go to an old email address you barely check.

- The lag is brutal. Escrow is based on last year’s bills. When taxes or insurance spike, you often do not feel it until the escrow analysis hits months later.

If you want “passive,” you need an owner-side system that catches these changes early and shows you what they do to cash flow per property.

What an escrow analysis is actually doing (and where the shortage comes from)

Your servicer runs an escrow analysis about once per year. The goal is simple:

- Look at what was actually paid out of escrow for property taxes and insurance.

- Project what will be paid out over the next 12 months.

- Add a cushion (servicers often keep a reserve so the account does not hit zero).

- Compare what you have to what you need.

If the account will not have enough money, you get an escrow shortage.

Rental owners usually get surprised for one of these reasons:

- Property taxes went up. Reassessment, higher millage, loss of an exemption, or a supplemental bill.

- Insurance went up. Premium increases, policy rewrite, non-renewal replacement, or force-placed insurance if a policy lapsed.

- Timing mismatch. Even if the annual total is right, a big bill due early in the year can trigger a shortage because the account has not accumulated enough yet.

If you want a quick gut-check, start with two questions: did taxes go up, did insurance go up. If either answer is yes, the escrow increase is usually real. The shortage piece is the “catch-up” for last year’s under-collection.

The two-part payment jump: higher escrow going forward plus the shortage spread

Your payment often increases for two separate reasons at the same time:

- Your ongoing escrow contribution increases because next year’s projected tax and insurance bills are higher.

- Your shortage is spread over time (commonly 12 months), adding a temporary monthly surcharge until the shortage is repaid.

This is also where rental cash flow gets destroyed quietly. A property that “cash flows $250 a month” on a spreadsheet can turn into $25 a month the day escrow resets.

A worked rental example (cash flow impact in real numbers)

Here is a clean example so you can see the math.

Assume a rental property was originally underwriting at:

- Rent: $1,700 per month

- Principal and interest (P and I): $1,050 per month

- Taxes: $2,400 per year ($200 per month escrow)

- Insurance: $1,200 per year ($100 per month escrow)

So the old payment was:

- P and I: $1,050

- Escrow: $300

- Total PITI: $1,350 per month

Now assume two things happen:

- Taxes increase by $600 per year (new taxes: $3,000, +$50 per month)

- Insurance increases by $900 per year (new insurance: $2,100, +$75 per month)

Your new baseline escrow needs to be:

- New escrow: $200 + $50 + $100 + $75 = $425 per month

But last year the servicer collected $300 per month and paid bills that ended up higher. That creates a shortage.

If the shortage is $1,200 and the servicer spreads it over 12 months, that is:

- Shortage spread: $100 per month for 12 months

So your new payment becomes:

- P and I: $1,050 (unchanged)

- New escrow: $425 (higher going forward)

- Shortage spread: $100 (temporary)

- New PITI: $1,575 per month

That is a $225 per month jump.

If your property was netting $300 a month after the PM, that single escrow analysis just cut your cash flow by 75 percent.

This is why rental owners need to track escrow as part of the loan system, not as a surprise letter you handle once per year.

The rental owner checklist: how to prevent escrow surprises across a portfolio

You cannot stop taxes and insurance from moving. You can stop getting blindsided.

Use this checklist as an owner-side operating rhythm.

1) Know your escrow analysis month for every loan

Every servicer has a computation year. If you do not know when it runs, you cannot predict when the payment will change.

At minimum, track the servicer name, the escrow analysis month, and when taxes and insurance renew each year.

2) Capture the three documents that explain 95 percent of “payment jumps”

If you are missing any of these, you are guessing:

- Escrow analysis statement

- Property tax bill (or assessment notice)

- Insurance declarations page (and renewal notice)

If those are scattered across PM inboxes and PDF folders, you will always be late.

3) Separate “the shortage” from “the new baseline”

When your payment jumps, ask two questions:

- How much is the temporary shortage spread, and when does it end?

- How much is the new ongoing monthly escrow, and what bill increased to cause it?

If you do not separate these, you will make bad decisions, like thinking a $180 increase is permanent when $80 of it drops off in 12 months.

4) Treat escrow changes like a cash flow event, not a paperwork event

Escrow changes are not just loan trivia. They change your monthly cash flow, your per-property P and L, and your DSCR if you finance with DSCR loans.

If you are only looking at your portfolio once per quarter, escrow resets can wreck you before you notice.

5) Audit your servicer’s inputs

Servicers are usually right, but “usually” is not good enough when you are scaling.

If your escrow analysis looks off:

- Compare the tax amount to the county bill

- Compare the insurance amount to the declarations page premium

If those inputs are wrong, request a re-run before you accept the new payment.

6) Build the one habit that makes this passive

You want a five-minute review habit, not a twelve-tab spreadsheet.

The habit is: every time a tax bill, insurance renewal, or escrow analysis shows up, it gets captured, categorized, and translated into what you actually care about.

That is what keeps this manageable as you scale.

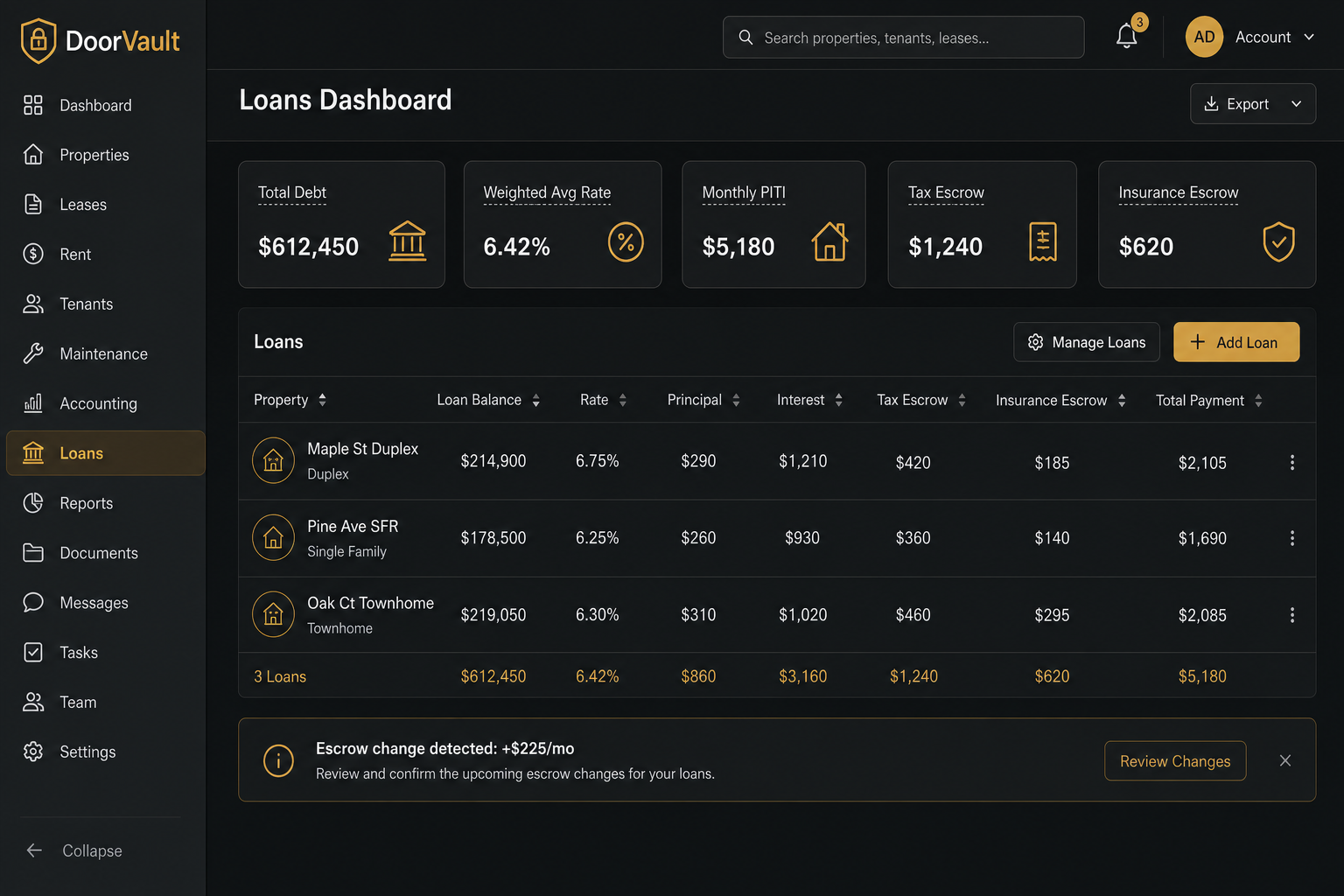

How DoorVault keeps your taxes, insurance, and loans clean without spreadsheets

This is exactly the kind of problem DoorVault is built for: owner-side operations for landlords who use property managers.

Knox Intelligence is AI that proposes, learns, and never touches your data without permission. You can keep it in review mode or let it apply changes automatically. Either way, the workflow stays the same: you forward, upload, or sync, and Knox does the back-office work.

Here is what that looks like for escrow volatility:

- Forward the email. Escrow analysis statements, mortgage statements, insurance renewals, tax bills, and invoices can all go to your Knox inbox.

- Knox reads the document and extracts the numbers. Taxes, premiums, renewal dates, and loan details get structured and tied to the right property and entity.

- Your Loans Dashboard updates automatically. PITI is split into principal, interest, tax escrow, and insurance escrow so you can see the real monthly burn.

- Your portfolio view stays honest. Per-property P and L and portfolio KPIs reflect the new reality without you retyping anything.

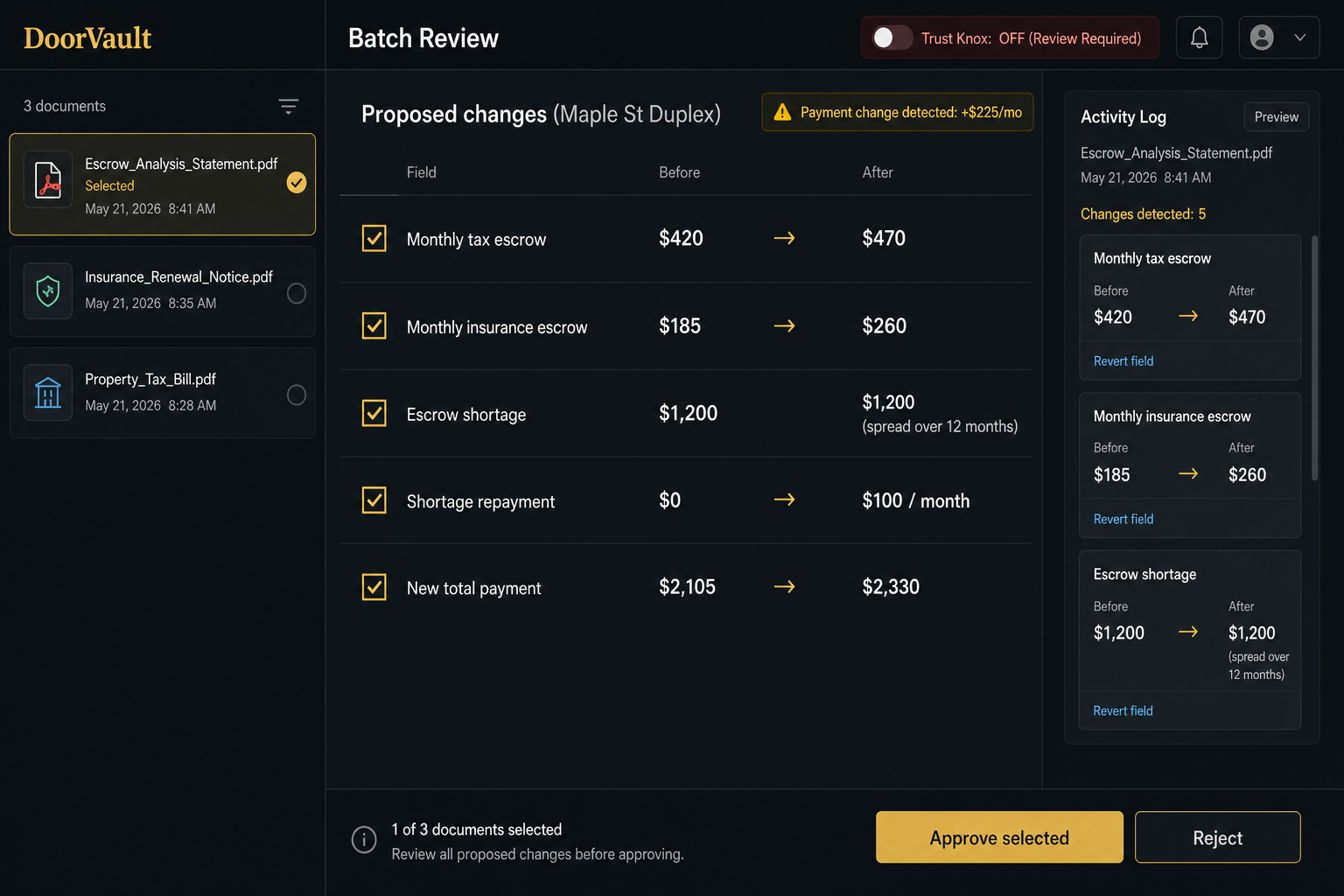

- Nothing changes silently. The Activity Log shows every change with before and after snapshots, and you can revert a single field if something is wrong.

This same workflow also keeps the rest of the owner side clean, like PM statement reconciliation, insurance renewal tracking, document organization, and tax-ready exports. If those are pain points for you, start here: Owner Statement Reconciliation and Landlord Insurance Checklist.

If you are scaling a portfolio, the goal is not to become an expert in escrow. The goal is to never have to think about escrow unless something is actually off.

CTA: stop getting surprised

Start free. 2 properties. No credit card. → https://doorvault.app