Should You Sell Your Rental Property at a Loss? Know NOI First

A bad month can make a decent property look guilty.

One vacancy. One repair. One reserve top up. One owner statement that feels worse than it actually is.

That is usually when the question shows up: should you sell your rental property at a loss?

Maybe. But not before the NOI is clean.

Selling can be the right call when the asset is truly broken, the market moved against you, or the capital has a better next home. It can also be an expensive reaction to bad records. The difference is not vibes. The difference is the owner side math.

The direct answer

Do not decide from the listing price, the last PM statement, or the emotional weight of one ugly month.

First calculate reconciled NOI. That means rent collected, vacancy, PM fees, repairs, insurance, taxes, utilities, reserves, and any recurring operating costs tied to the property. Then match the PM payout to the bank deposit and separate operating performance from debt service.

If the clean NOI is weak, the sale proceeds are better redeployed elsewhere, and the tax picture works with your CPA, selling at a loss may be rational.

If the property still has stable NOI but your statements are messy, selling may punish the asset for a back office problem.

There is also a tax layer. Rental property losses can be treated differently than personal home losses, and the IRS has rules around capital gains and losses. A tax guide can explain the broad mechanics, but your CPA should model the actual sale. The operating decision starts before that. It starts with whether the property is actually failing.

Your PM statement is not the whole truth

A PM statement is useful. It is not the whole record.

The owner statement tells you what the PM says happened. The bank deposit tells you what cash actually arrived. The invoices, leases, mortgage statements, insurance renewals, and tax bills tell you whether the statement labels are complete.

Say a property collects $1,650 in rent.

The statement shows:

- PM fee: $165

- Repair: $410

- Reserve top up: $150

- Owner payout: $925

Then the bank shows an $875 deposit.

That $50 gap matters. It may be a correction, an owner charge, a timing issue, or a missing row. But until you name it, the property math is not clean.

That is how owners make bad sell calls. They react to the feeling of a thin payout instead of the reason behind it.

NOI is where the drama gets boring

NOI is operating income minus operating expenses before debt service.

That part matters. Debt can make a property cash flow tight even when the asset itself is producing. A bad loan, escrow jump, or high rate may be the problem. The rental may still be doing its job.

Here is a plain version:

Monthly rent: $1,650

Average vacancy allowance: $80

PM fee: $165

Taxes: $210

Insurance: $155

Average maintenance: $120

That leaves about $920 in monthly NOI before debt.

If principal and interest are $910, the owner sees almost no monthly cash flow. One $1,200 repair turns the month negative and makes the property feel broken.

But the sale question is different.

Is the property failing, or is the debt structure tight? Was the repair recurring, or was it a one time hit? Is the PM padding reserves, or did the bank deposit actually match? Is rent below market, or is the market telling you the property has no pricing power?

NOI turns panic into questions you can answer.

The sell decision needs 5 records

Before you list a rental at a loss, pull 5 records:

- The last 12 months of PM statements

- The matching bank deposits

- The repair invoices and major expense proof

- The loan payoff, escrow, and debt service details

- A realistic sale cost estimate

Now run the property in two lanes.

Lane one is asset performance. Rent, vacancy, operating costs, recurring repairs, PM fees, taxes, insurance, and true NOI.

Lane two is capital outcome. Payoff, closing costs, taxes, cash released or cash needed to close, and what that capital can do next.

This is where a loss can still make sense. If selling frees trapped capital and lets you redeploy into a stronger deal, the loss may be the price of exiting a weak asset. If selling forces you to bring cash to closing while the property still has stable NOI, the better move may be to fix the records, refinance later, adjust rents, replace the PM, or hold.

The answer is not always hold. It is not always sell. It is know the number before you pick a side.

How DoorVault runs the owner side

DoorVault is built for investors who use property managers but still need to run the asset.

Forward any property related email to Knox. PM statements, repair invoices, insurance renewals, tax bills, mortgage statements, closing docs, leases, inspection reports, anything tied to the property. Knox reads the documents, files them to the right property, and proposes the transactions for review.

For a sell versus hold call, that means the numbers stop living in six places.

DoorVault reads PM statements line by line, matches owner payouts to bank deposits, keeps per property P&L current, tracks loan balances and equity, stores the supporting documents, flags unusual expenses, and gives you the sell versus hold view from actual portfolio data.

The same system also supports Schedule E export, CPA access, entity reporting, Section 8 records, BRRR pipeline tracking, lender packages, insurance tracking, and portfolio health scores.

That breadth matters because a sell decision is rarely one number. It is cash flow, documents, debt, taxes, PM behavior, equity, and capital strategy tied together.

The 30 minute test before you list

Before you call an agent, do this:

- Rebuild the last 12 months of rent and operating expenses.

- Match every PM payout to the bank deposit.

- Separate recurring repairs from one time repairs.

- Calculate NOI before debt service.

- Calculate cash flow after debt service.

- Pull the loan payoff and estimated sale costs.

- Ask where the released capital goes next.

If the clean numbers still say the asset is weak, selling can be a disciplined move.

If the property looks bad only because the PM statement, bank deposit, loan, and documents do not agree, you do not have a sell decision yet. You have cleanup.

The point is not to keep every rental forever. The point is to stop making capital decisions from incomplete data.

FAQ

Is there a tax benefit to selling a rental property at a loss?

There can be, but it depends on how the property was used, depreciation, basis, passive activity rules, and your broader tax picture. Talk to a CPA before selling. DoorVault helps keep the operating records and tax package clean so the tax conversation starts with better data.

What number should I know before selling a rental property?

Start with trailing 12 month NOI, then cash flow after debt service, then net sale proceeds after payoff and closing costs. If those three numbers are not clean, the sell versus hold call is not ready.

Can DoorVault help me decide whether to sell or hold?

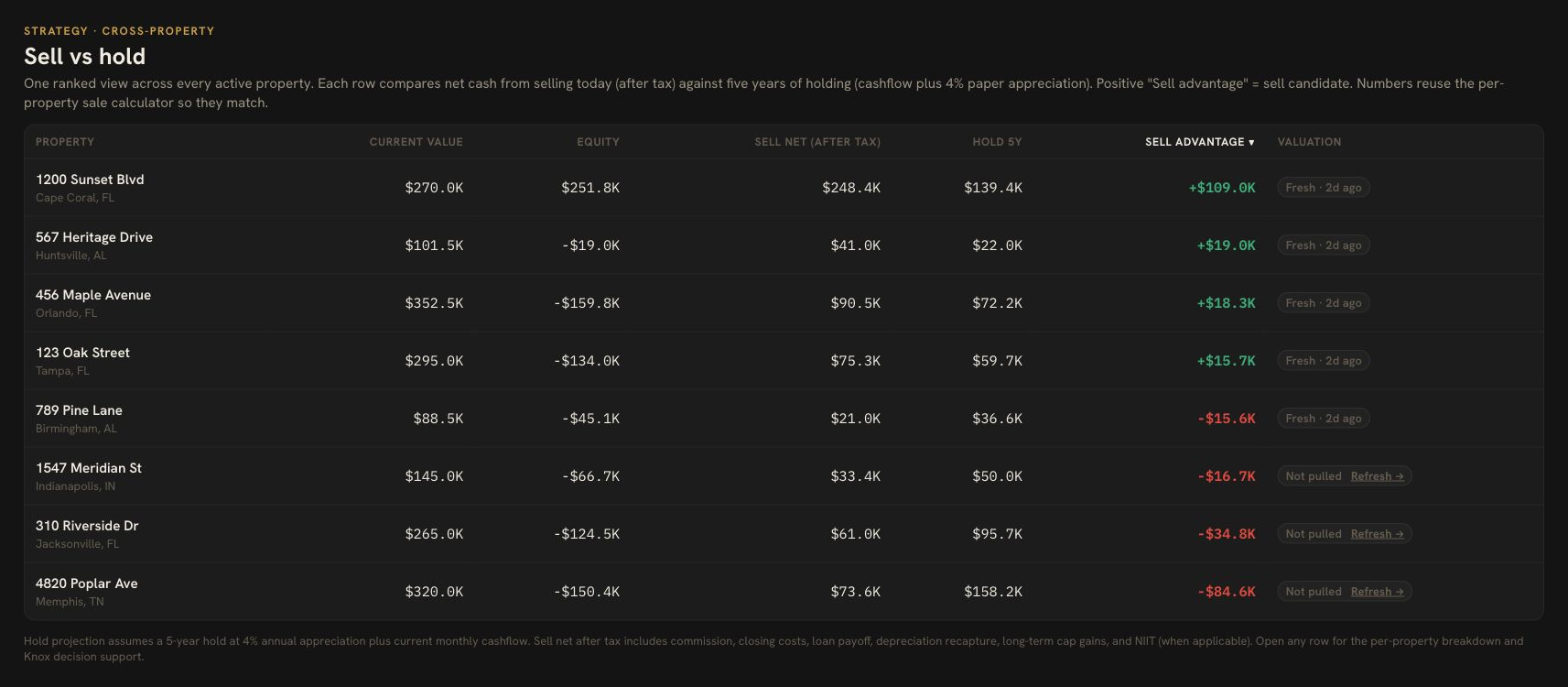

DoorVault gives you the records that make the decision real: PM statements, bank deposits, P&L, debt, equity, documents, and sell versus hold analysis in one place. You still make the call. You stop guessing from scattered PDFs.

Still making sell versus hold calls from a PM PDF? Start free at https://doorvault.app.