Section 8 Deal Analysis: FMR Is Not the Deal

Section 8 deal analysis gets stupid fast when the rent number looks good.

A 3 bedroom FMR says 1,583 dollars. The asking price is 95,000 dollars. Somebody whispers cashflow and everyone starts acting like the spreadsheet paid for closing costs.

It did not.

FMR is one input. Not the deal.

A rent lookup is not underwriting

HUD Fair Market Rent matters because it helps set the payment standard for Housing Choice Voucher rents. HUD describes FMR as its estimate of the 40th percentile rent for recent movers in a market, and local housing authorities often set voucher payment standards around that number.

That sounds official because it is.

It also does not mean your property will be approved at that rent.

The housing authority still has to look at bedroom count, utilities, rent reasonableness, tenant portion, local payment standards, and the actual condition of the property. HUD explains that the housing assistance payment is based on the payment standard and the tenant portion. A 1,583 dollar FMR does not tell you whether the unit passes inspection. It does not tell you whether the tenant can afford their portion. It does not tell you whether your PM will get the lease up done in 30 days or 75 days.

That is why treating FMR as the verdict is lazy underwriting in a nice shirt.

Use the FMR lookup. Then make the number survive the rest of the deal.

If you want the cleaner mechanics first, read the Section 8 Fair Market Rent guide or use the Section 8 FMR lookup. Then come back to the actual math.

The first pass has 5 gates

The first pass should be boring.

That is how you know it works.

For BRRR Section 8 deals, Eduardo does not start with vibes. The hard gates are:

- At least 20 percent equity after purchase plus rehab.

- At least 150 dollars per month in cashflow after expenses.

- At least 1,150 dollars in rent.

- No more than 75,000 dollars in rehab.

- At least 350 square feet per bedroom.

Then he adds the personal floor that matters for his strategy: at least 15 percent cash on cash for BRRR Section 8 deals.

Notice what is missing.

No single cap rate flex.

No screenshot of a huge gross yield.

No pretend certainty because the rent table looked friendly.

A deal with 18 percent equity is a near miss, not a victory lap. A deal with 21 percent equity can still fail if cashflow drops below 150 dollars after the refi loan steps down. A deal with a beautiful rent number can still be garbage if the rehab eats 82,000 dollars and ties up capital for a year.

That is the point of gates.

They kill the deal before the deal kills your year.

Capital velocity beats a pretty cashflow screenshot

Most deal analysis tools love the cashflow number because it looks good on a card.

Cashflow matters.

Capital trapped matters more when you are trying to scale.

Here is the clean example.

Deal A recovers all your capital at refinance and cashflows 180 dollars per month.

Deal B traps 25,000 dollars in the property and cashflows 350 dollars per month.

Most investors screenshot Deal B.

The operator buys Deal A.

Because Deal A gives you your money back. That money buys the next property. Then the next one. Then the next one after the PM sends a statement with three line items named maintenance and zero invoices attached. Cute.

This is why DoorVault looks at more than rent, price, and cashflow. DoorVault’s Deal Underwriting Engine tracks equity created, capital recycled, cashflow above the floor, rehab simplicity, and velocity rating. The BRRR Pipeline keeps acquisition, rehab, rent, refinance, and repeat in one view, with rehab budget versus actual and refinance readiness tied to the same property record.

For the deeper math, the capital velocity real estate guide is the better rabbit hole.

The deal still has to live after closing

Buying the property is not the hard part.

Keeping the numbers clean after a PM, a housing authority, a lender, and a CPA all touch the same asset is the hard part.

That is where most Section 8 analysis tools stop too early.

They answer the pre purchase question:

“Does this deal work?”

Fine.

But the asset keeps asking questions after closing:

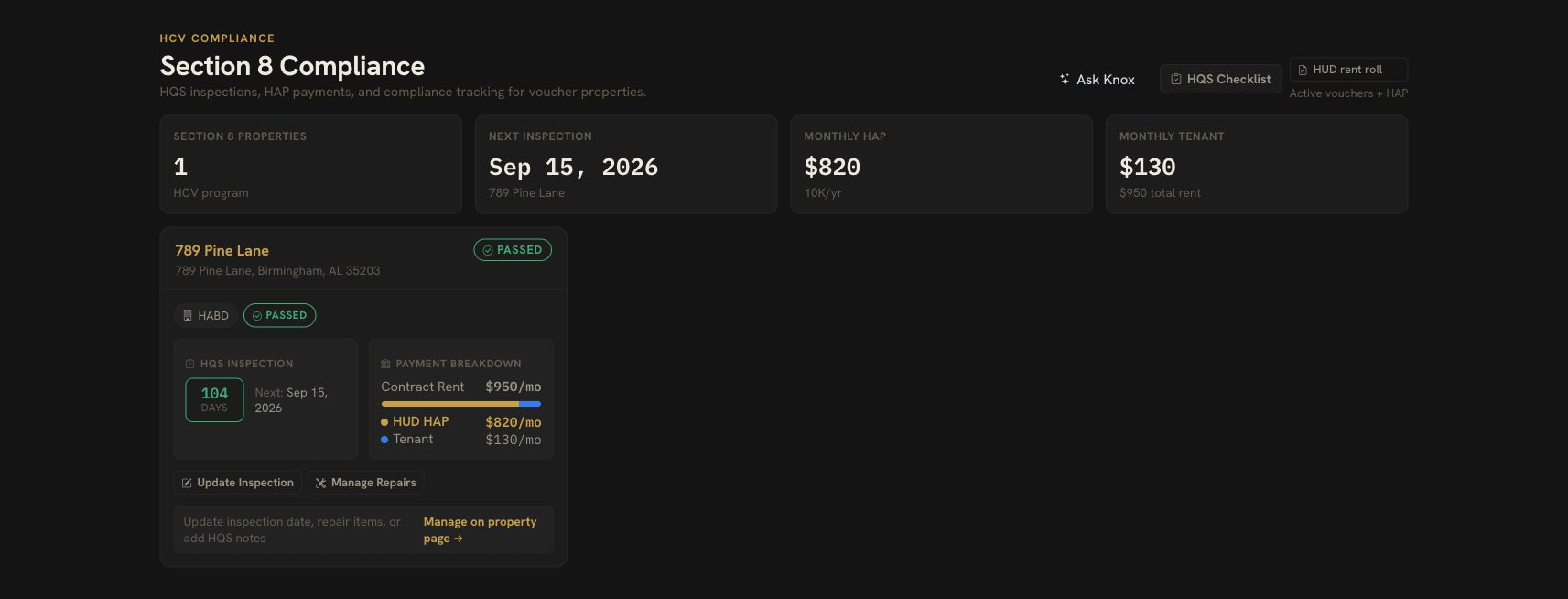

- Did the HAP payment arrive at the approved amount?

- Did the tenant portion post?

- Did the inspection deadline move?

- Did the PM statement match the bank deposit?

- Did the repair invoice belong to this property or the one two streets over?

- Did the mortgage payment split correctly between principal, interest, tax escrow, and insurance escrow?

- Did the year end records land in the right Schedule E bucket?

That is not a calculator problem.

That is an owner side system problem.

DoorVault is built for that whole chain. Knox Intelligence proposes, learns, and never touches your data without permission. Forward any property related email, upload a closing doc, or sync a folder. Knox reads the documents, files them to the right property, creates transactions, and keeps the audit trail.

For Section 8 specifically, DoorVault tracks vouchers, HAP portions, tenant portions, inspection dates, FMR limits, and repair follow ups. PM Statement Processing reads every owner statement line. Bank Reconciliation and Plaid Smart Sync match deposits to the statement. The Loans Dashboard keeps debt, LTV, DSCR, and payment splits visible. Equity Tracker and Refinance Analysis keep the refi math honest. Schedule E Export and the CPA Portal keep tax season from becoming a document scavenger hunt.

That is the difference between a deal score and an asset management platform.

One gives you a verdict.

The other keeps the verdict honest after the purchase.

The 10 minute Section 8 deal review

Here is the version worth saving.

Do this before you fall in love with the rent number:

- Pull FMR and the local payment standard context.

- Use the low rent, not the happy rent.

- Use the real rehab number, not the seller version.

- Check equity after purchase plus rehab.

- Check cashflow after PM fee, taxes, insurance, vacancy, maintenance, and debt.

- Step down refi LTV until cashflow clears 150 dollars.

- Check capital left in the deal.

- Check whether the property can pass inspection without another surprise rehab round.

- Decide whether this deal gets you to the next deal faster.

- If it passes, track the HAP, inspection, PM statement, loan, equity, and tax record from day 1.

That last line is where the money is.

Not because tracking is exciting.

Tracking is aggressively not exciting.

But missed HAP payments, fuzzy repair invoices, escrow drift, and stale refi math quietly eat the return you thought you bought.

Section 8 can be a strong strategy. Eduardo is actively scaling the Section 8 side of his portfolio in Birmingham for a reason. The mistake is treating the voucher rent as the whole thesis.

The real thesis is stricter:

Can the deal clear the gates?

Can the capital recycle?

Can the owner side stay clean after the PM takes over?

If the answer is yes, now you have something.

If you want DoorVault to run the deal analysis, FMR context, documents, HAP tracking, PM statements, loans, equity, and tax records in one place, start free with up to 2 properties at https://doorvault.app.

FAQ

What is Section 8 deal analysis?

Section 8 deal analysis is the process of checking whether a rental property can work with voucher rent. It should include FMR, payment standards, rent reasonableness, purchase price, rehab, inspection risk, cashflow, equity, refi math, and capital left in the deal.

Is Fair Market Rent the same as approved Section 8 rent?

No. FMR is a HUD rent benchmark. Local payment standards, utilities, rent reasonableness, bedroom count, tenant portion, and housing authority approval still matter.

What cashflow floor does Eduardo use for BRRR Section 8 deals?

The hard floor is 150 dollars per month after expenses. Eduardo also uses a personal 15 percent cash on cash minimum for BRRR Section 8 deals.

What makes a Section 8 deal fail?

A deal can fail because equity is below 20 percent, cashflow is below 150 dollars per month, rent is below 1,150 dollars, rehab is over 75,000 dollars, the layout is too small, or the property cannot pass inspection without blowing up the budget.