Landlord Insurance Checklist: 12 Gaps Your Property Manager Probably Hasn’t Flagged

If you are a landlord using a property manager, it is easy to assume insurance is handled. The declarations page is in a folder somewhere. The premium gets paid. The escrow analysis shows up once a year.

That is exactly how landlords discover an insurance gap at the worst possible time. A claim. A lender request. A renewal that jumps your payment. A vacancy clause you did not realize you triggered.

This landlord insurance checklist is written for the owner side of the business. Your PM can coordinate repairs. You still own the risk.

The mindset shift: insurance is an owner asset problem

Insurance does not fail because you “did not buy insurance.” It fails because your portfolio produces paperwork and deadlines that get scattered:

- Renewal notices land in the wrong inbox

- Vendor certificates of insurance never make it into a file you can find

- Policies are written to the wrong named insured after you move properties into an LLC

- Coverage limits drift while rebuild costs go up

- Vacancies happen and nobody flags the insurance consequence

If you own more than a couple properties, the operational problem is not knowing what landlord insurance is. The operational problem is keeping insurance clean across your whole portfolio while a PM sits between you and the day to day.

The fix is simple in theory. One system where insurance documents live. One place where renewal dates are tracked. One workflow where every update is auditable.

The 12 gaps to check before your next renewal

Use this checklist as a risk audit. None of these are “gotchas.” They are the boring gaps that turn into expensive surprises.

-

Wrong policy type for how the property is used

If you converted an owner occupied property into a rental, confirm you are not still on the wrong form. The claim denial stories are real. -

Named insured does not match reality

If the property is held in an LLC, confirm the policy is written correctly. The right answer depends on your structure, but the wrong answer is guessing. -

Your PM is not listed correctly

If your PM needs to be listed as additional insured or additional interest, confirm it is done and saved in writing. “They said it is fine” is not documentation. -

Dwelling limit is based on purchase price, not rebuild cost

Replacement cost is not what you paid. Rebuild cost moves. If your limit has not been revisited, it is probably stale. -

Deductible is out of sync with your reserves

A low deductible feels safe until your premium climbs. A high deductible is fine until you realize you cannot comfortably write the check. -

Loss of rent coverage does not match your actual rent

If the property is down for repairs, the rent you lose is not theoretical. Confirm the limit and how long it pays. -

Vacancy clause exposure

Many policies restrict coverage after a unit sits vacant beyond a threshold. Your PM may think “vacant” is an operational status. Your insurer thinks it is a risk condition. -

Ordinance or law coverage is missing

If a claim forces you into code upgrades, the gap is real. This is one of the most common surprises on older properties. -

Water backup, sump, and plumbing exclusions you never read

Most landlords learn what is excluded only after the mess happens. Do the unglamorous reading now. -

Vendor COIs are not collected and tracked

Roof. HVAC. Plumbing. Tree work. If a vendor gets hurt or causes damage, you want clean coverage lines and a paper trail. -

You cannot find the policy in under 30 seconds

If it takes a 15 minute inbox search, you do not have insurance organized. You have insurance somewhere. -

Your insurance data is disconnected from your numbers

Premium changes hit NOI. Escrow changes hit cash flow. If you only notice at tax time, you are managing late.

The owner workflow that prevents these gaps

The checklist is the diagnosis. The solution is a repeatable workflow that works even when you have a PM.

Here is the simplest version:

-

Centralize every insurance related document

Declarations. Renewal notices. Paid invoices. COIs. Claim letters. Lender proof requests. Put them in one place. -

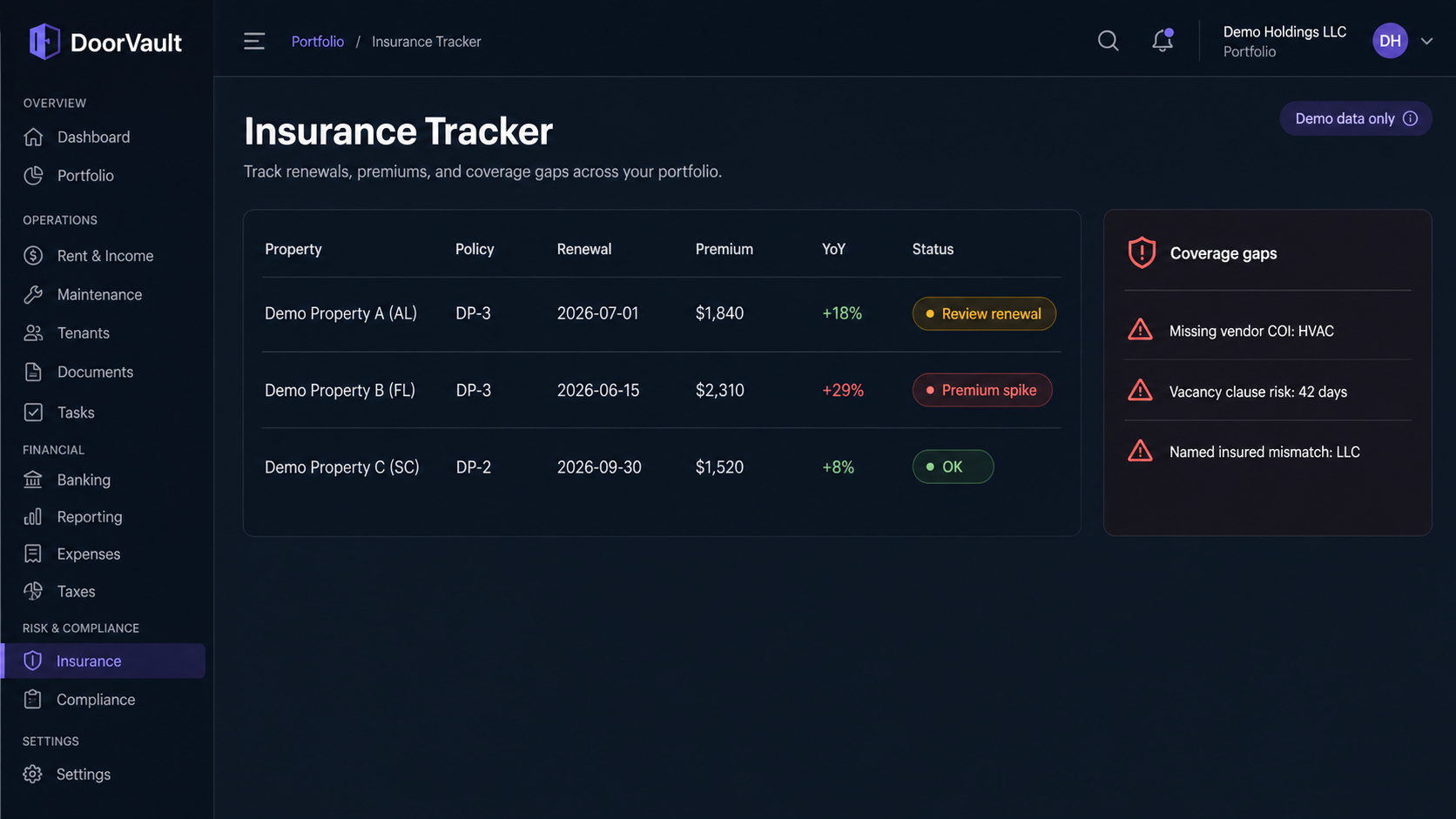

Track renewal dates and expiration dates like a compliance deadline

If you only think about insurance at renewal time, you will always be rushed. -

Tie insurance changes to portfolio performance

Premium up. Deductible change. Coverage shift. Those are not “insurance admin.” They are portfolio inputs. -

Keep an audit trail

When a policy gets updated, you need to know what changed, when it changed, and who approved it.

This is the part spreadsheets and shared folders never solve. They store files. They do not run the workflow.

How DoorVault keeps insurance clean when you have a PM

DoorVault is built for landlords who use property managers but still need to run the investor side. The workflow is straightforward:

- Forward any property related email to your Knox inbox, upload documents, or sync a cloud folder

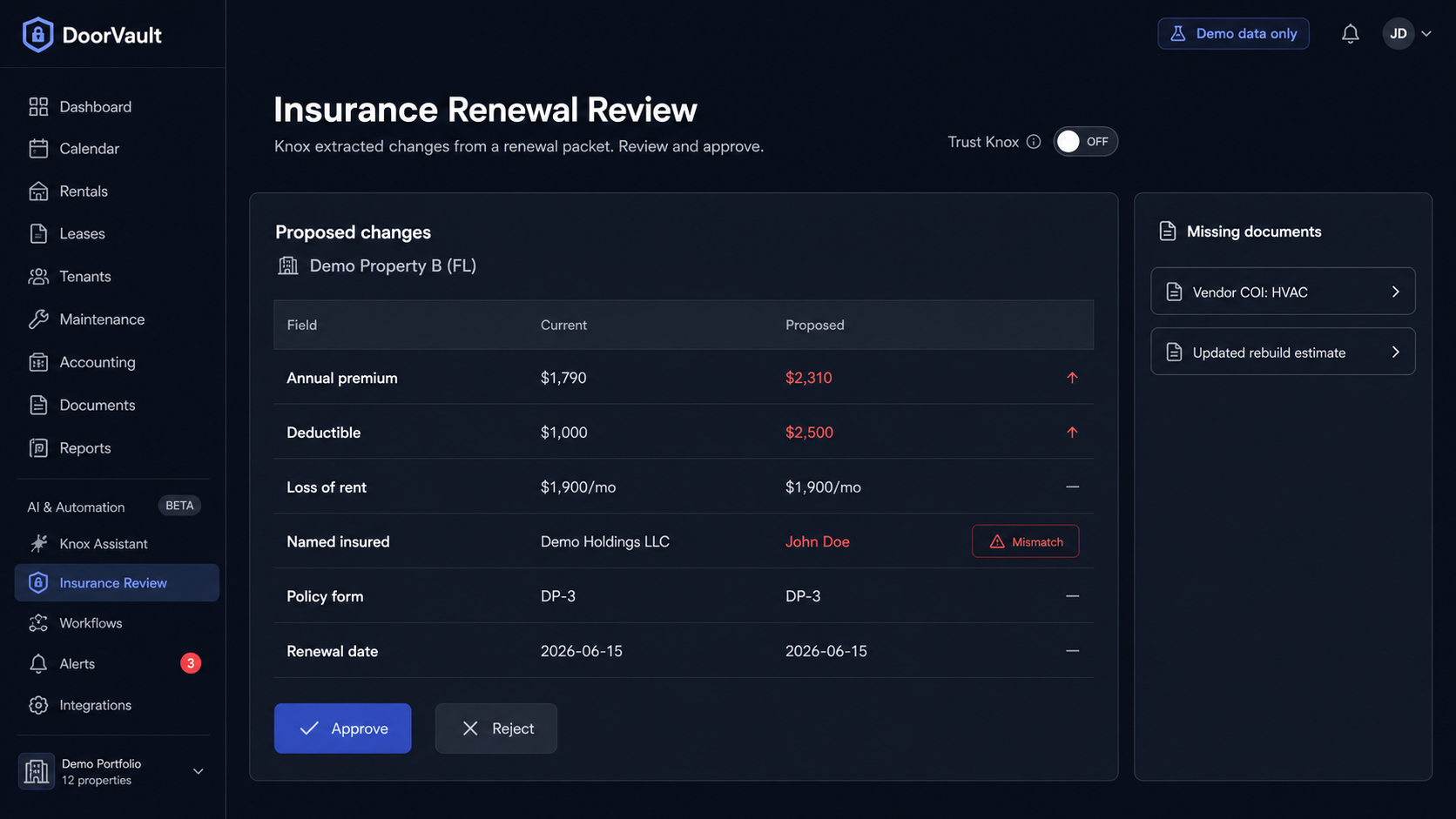

- Knox reads documents, extracts the fields that matter, and files them to the correct property

- If you want control, Trust Knox can be off so every change is proposed for approval first

- Every change is recorded in the Activity Log with before and after snapshots, with a one click revert

For insurance, that means a renewal notice is not just a PDF. It becomes data:

- Renewal date tracked

- Premium stored and compared to prior policy

- Coverage limits captured

- Missing items flagged

And it does not stop at insurance. This is where the platform breadth matters:

- Premium changes flow into reporting so you see the NOI impact

- Loan and escrow changes are tracked alongside insurance, not in a separate spreadsheet

- Vendor invoices can be captured and categorized correctly for tax season

- Entity level reporting stays clean when properties are held across multiple LLCs

Why this is really a portfolio system problem

Insurance is one pillar. But the reason it breaks is the same reason everything breaks at scale. Owner side work gets fragmented:

- PM statements live in one portal

- Insurance renewals live in email

- Loan statements live in a servicer login

- Tax prep lives in a folder you dread opening

DoorVault is designed to connect those owner side pieces in one place. Not as a “tracking tool.” As an operating system for a rental portfolio that is supposed to be passive.

If you want a quick self test, answer this without searching:

- Which properties renew in the next 60 days?

- Which policy had the biggest premium jump this year?

- Which vendor COIs are missing right now?

If you cannot answer quickly, the fix is not working harder. The fix is a system that collects the documents, extracts the data, tracks deadlines, and shows you the owner actions that matter.

Start free. 2 properties. No credit card. → https://doorvault.app